One officer of a Company said, “If I had known he needed money, I would have loaned it to him”. Another asked, “How could this happen”? And yet another exclaimed, “We are ruined! We can’t make payroll!” All of these are reactions to the discovery of fraud in their Company. Hindsight will eventually bring us to ask WHY did this happen. What are the motivations for our employees in considering committing these crimes? In response, I want to discuss two of my favorite theories.

During the 1940’s Dr. Donald Cressey, then a PhD candidate, interviewed 200 embezzlers. Dr. Cressey developed the fraud triangle as an integral part of his hypothesis.

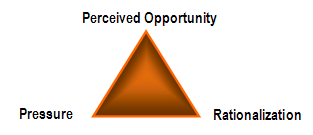

Cressey’s Fraud Triangle:

The pressure is a non-sharable financial need. This factor alone is what turns otherwise honest people into fraudsters. Examples of pressures include excess credit card debt, medical bills, drug addictions, gambling, and divorce. Although there are others, these serve for illustration here. My point is that as people’s positions in life change, their actions do also, and sometimes to their detriment. This is why even the “honest” cannot be fully trusted.

The rationalization is the explaining away, at least to themselves, a plausible justification for their fraud. Justifications can include; I am not paid enough, I am only borrowing it, and I was passed over for a raise I deserved. This makes the crime palatable to the fraudster, to the point where they feel no guilt whatsoever.

The perceived opportunity is essentially access to the target of their gain. Examples of access include; being a signer on the business’s checking account, and physical access to cash or inventories. Cressey noted that the job of the individual has a direct connection to the type of fraud committed. Cashiers skim or lap cash, accountants use checks and journal entries, and bankers loan money to fictitious borrowers.

The perceived opportunity is essentially access to the target of their gain. Examples of access include; being a signer on the business’s checking account, and physical access to cash or inventories. Cressey noted that the job of the individual has a direct connection to the type of fraud committed. Cashiers skim or lap cash, accountants use checks and journal entries, and bankers loan money to fictitious borrowers.

Cressey noted that all three factors were necessary in order for a fraud to occur; the opportunity, then the pressure, and finally the rationalization.

Cressey noted an exception to his theory, that of the pathological offender. The pathological offender obtains his job solely for the purpose of committing a fraud. These offenders have most likely committed a similar offense at a previous employer. (Cressey: ACFE, Kranaher)

Another theory is The Routine Activities Theory. This theory states that there will always be a certain number of people in the population who are motivated to commit a crime. Motivations include greed, lust, and evil. Whether a crime occurs or not, as well as the severity of the crime, is more dependent on the activities of the victims or potential victims.

An example of this theory would state that there would always be people motivated to steal automobiles. The car owner who leaves his vehicle outside, unlocked and with the keys in it, is more apt to become a victim of car theft than is the owner who locks his vehicle in his garage, and has an alarm on the garage and the vehicle. So, the activity of the victim or the protection or defense characteristics used is the variable as to whether a crime is committed, or not, under this theory.

Under this theory, there are three elements that influence crime:

- The availability of victims.

- The absence of oversight.

- The availability of motivated offenders. (Routine Activities Theory: ACFE)

Let me summarize to this point. Generally the “honest” people cannot be trusted, because people’s situations can change, which then creates the pressure in Cressey’s theory. Pathological offenders who commit crime for the sake of the crime exist. Provided you accept the Routine Activities Theory, the victim has an active role in crime.

There are a few things a business can do. It was Ronald Regan who stated “trust, but verify” when it came to monitoring an arms agreement with the Russians. This same approach can be very valuable in protecting a business from fraud. Monitoring activities in a simple case is many times reviewing payroll reports, bank statements, and other reports generated by your accounting software. Avoid situations where the same individual can initiate, authorize and record a transaction. Do not pre-sign checks for convenience sake. Do not use signature stamps. Get a fiduciary bond for those handing your accounting and your cash. During the bonding process, a background check is usually performed. Finally, get help. In each of these examples above, a professional evaluation of the fraud risks and internal controls would have saved the business significant amounts of money.

If you have concerns, please contact author Robert Kenific, Jr., CPA, CFE for an evaluation specific to your situation, at (908) 782-7900 or email rk@bkc-cpa.com